“Is there something better I could do with my money?”

Many people approaching retirement find themselves wondering, “Do I need an annuity?” But beneath that question is often a deeper one: “Is there something better I could do with my money?”

It’s a fair concern—and one worth addressing. After all, the goal in retirement planning isn’t to pick the flashiest product; it’s to build a plan that provides confidence, security, and peace of mind.

Start With the Purpose, Not the Product

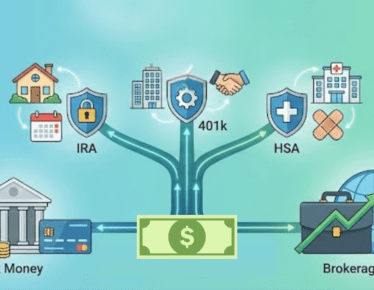

Before comparing annuities to other options like CDs, MYGAs, stocks, or real estate, it’s essential to define the problem you need to solve.

Every financial product serves a primary purpose

- Some are designed to grow assets safely

- Others are designed to generate guaranteed income for life

Annuities often try to do both, but one goal usually takes priority. Choosing between an annuity and an investment account isn’t about which is “better,” but about which tool is more appropriate for the specific job at hand.

Understanding Income-Focused Annuities

When the goal is guaranteed lifetime income, annuities become particularly relevant. There are three main types of income-generating annuities:

- SPIAs (Single Premium Immediate Annuities)

- DIAs (Deferred Income Annuities)

- Fixed Indexed Annuities with income riders, often referred to as “hybrid pensions”

These products can provide a contractual, written guarantee of income for life, regardless of market performance or lifespan.

But What About Investment Income?

Investments such as dividend-paying stocks, REITs, mutual funds, and real estate can certainly produce income. However, investment-based income is typically variable and subject to market risks.

Relying solely on market-driven income in retirement is similar to accepting a job where the paycheck reflects stock market performance that week. Most wouldn’t feel comfortable with that kind of uncertainty, especially when covering basic living expenses.

That’s why a balanced plan often includes both investment growth potential and secure, guaranteed income.

Why Guaranteed Income Impacts Happiness (and Longevity)

Research consistently shows that guaranteed income not only provides financial stability but also contributes to overall well-being.

Economist and retirement researcher Tom Hegna cites multiple studies (including one by the University of Chicago) that found retirees with lifetime income annuities:

- Experience less stress

- Are less affected by market downturns

- Tend to live longer

- Report higher levels of happiness

According to a Wall Street Journal article he referenced, the happiest retirees weren’t necessarily the wealthiest—they were the ones with pensions or fixed annuity income. Teachers, firefighters, government employees, and military retirees—those with dependable paychecks in retirement—are often among the most content.

This sense of predictability and control can have real emotional and physical health benefits in retirement.

Annuities and Historical Context

Annuities are not new. They date back to the Roman Empire. Social Security and employer pensions are also forms of annuities. What makes them unique is that contracts, not market projections, back them.

Only insurance products can legally guarantee income for life in writing. That’s why Social Security is funded through the Federal Insurance Contributions Act (FICA)—emphasis on insurance.

What About Market Risks?

Indeed, investments often have higher upside potential. However, that potential comes with risks:

- Market risk

- Longevity risk (outliving savings)

- Inflation risk

- Sequence-of-returns risk

- Emotional and health-related stress

Annuities help mitigate many of these concerns, offering peace of mind for a portion of one’s retirement income.

The Smarter Question to Ask

Rather than asking, “Do I need an annuity?”, a better question might be: “How much of my retirement income should be guaranteed—and at what age should I consider an annuity?”

This question shifts the focus from the product itself to the broader strategy. For many, combining annuities with investments and other income sources can provide the optimal balance of security and growth.

Final Thoughts

Annuities aren’t for everyone. But for those seeking predictable, lifelong income—especially as a replacement for a paycheck—they can be a powerful piece of a well-rounded retirement plan.

Different financial tools serve various purposes. The key is understanding what each one is meant to do, and choosing based on personal goals, risk tolerance, and lifestyle preferences—not fear, hype, or outdated assumptions. We can help. Let’s start a conversation today.

Contact Us Get in Touch

Have a question or feedback?

Fill out the form below, and we’ll respond promptly!

By providing your name and contact information, you are consenting to receive calls, text messages, and/or emails from a licensed insurance agent about Medicare Plans at the number provided. You agree that such calls and/or text messages may use an auto-dialer or robocall, even if you are on a government do-not-call registry. This agreement is not a condition of enrollment.

Not connected with or endorsed by the United States government or the federal Medicare program. This is a solicitation of insurance, and your response may generate communication from a licensed producer/agent.