Qualified vs. Non-Qualified Funds: What’s the Difference?

Understanding the difference between qualified and non-qualified retirement accounts is one of the most important foundations of tax-efficient retirement planning.

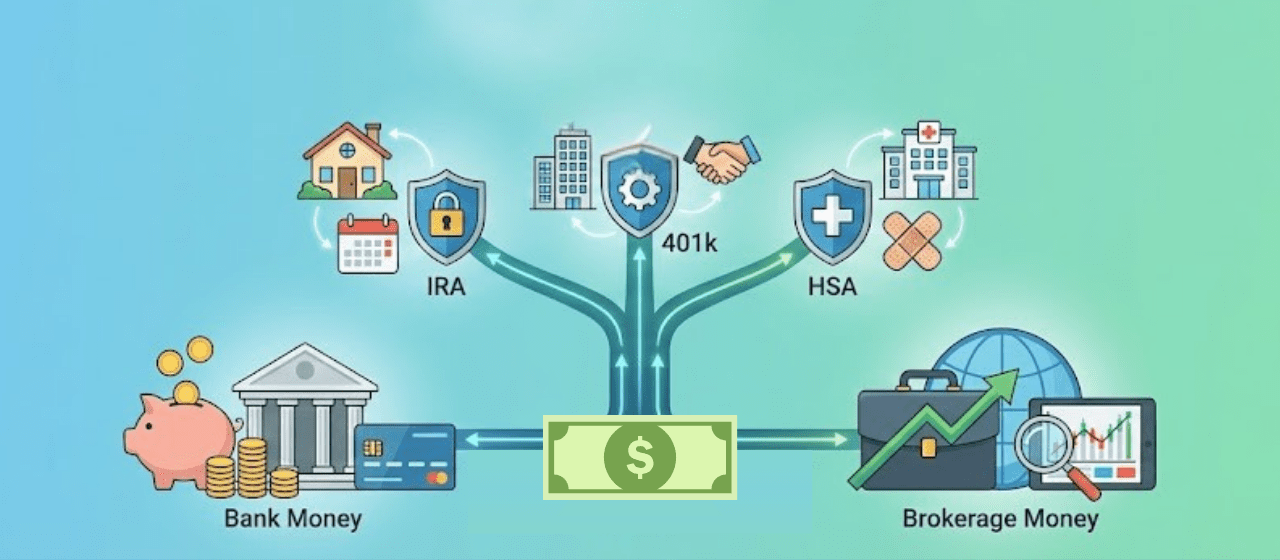

Most people save for retirement across multiple account types — 401(k)s, IRAs, brokerage accounts, Roth accounts, annuities, and more. But few understand how these accounts are classified or how that classification affects taxes, withdrawals, and long-term income planning.

In this guide, we’ll break down:

-

What qualified retirement accounts are

-

What non-qualified funds are

-

How each is taxed

-

How withdrawals work

-

Why account classification matters in retirement

-

Where Hybrid Pensions fit into the equation

How Retirement Accounts Are Classified

Retirement savings fall into two main categories:

-

Qualified Funds

-

Non-Qualified Funds

The difference primarily comes down to tax treatment and IRS rules.

Qualified accounts receive special tax advantages under IRS retirement law. In exchange, they come with contribution limits, withdrawal restrictions, and required minimum distribution (RMD) rules.

Non-qualified accounts do not receive special retirement tax treatment — but they offer greater flexibility and fewer restrictions.

Most retirees use both. Understanding how they interact can significantly improve retirement income planning and tax control.

What Are Non-Qualified Funds?

Non-qualified funds are dollars that have already been taxed and are saved outside of retirement accounts. These funds commonly include brokerage accounts, savings accounts, CDs, money market accounts, and other after-tax investment accounts. Some annuities can also be funded using non-qualified money.

Because non-qualified funds are not governed by IRS retirement rules, they come with fewer limitations. There are no contribution limits, no age-based withdrawal requirements, and no required minimum distributions. This flexibility can be especially valuable in retirement, when managing income and taxes becomes more important.

Common examples include:

-

Brokerage accounts

-

Savings accounts

-

CDs and money market accounts

-

After-tax investment accounts

-

Certain annuities funded with non-qualified money

Because non-qualified funds are not governed by retirement account rules:

-

There are no contribution limits

-

There are no age-based withdrawal penalties

-

There are no required minimum distributions

Strategically using non-qualified funds alongside qualified withdrawals can help manage marginal tax brackets — something we discuss further in our guide on the Accelerated RMD 5-Bucket Strategy.

How Non-Qualified Funds Are Taxed

Since non-qualified contributions were already taxed:

-

You are not taxed again on principal

-

You are taxed only on earnings or gains

Tax treatment depends on the investment:

-

Long-term capital gains may receive preferential tax rates

-

Interest income may be taxed as ordinary income

-

Annuities follow different distribution rules (often LIFO — last in, first out)

This flexibility allows retirees to better control taxable income in a given year — particularly before RMDs begin or when coordinating Social Security.

If you’re exploring annuities as part of your after-tax strategy, our guide on Are Annuities Right for You? can help clarify the role they play.

What Are Qualified Funds?

Qualified funds are money saved inside retirement accounts that receive special tax advantages under IRS rules. These accounts are designed to encourage long-term retirement savings, which is why they come with contribution limits, withdrawal rules, and age-based requirements.

For many people, qualified accounts make up the largest portion of their retirement savings because of employer-sponsored plans and years of tax-deferred growth.

These accounts are designed to encourage long-term retirement savings, which is why they include:

-

Annual contribution limits

-

Early withdrawal penalties

-

Required Minimum Distributions (RMDs)

-

Specific eligibility rules

For many households, qualified accounts represent the majority of retirement savings.

Common Types of Qualified Retirement Accounts

Traditional IRA

A Traditional IRA is typically funded with pre-tax or tax-deductible contributions.

-

Growth is tax-deferred

-

Withdrawals are taxed as ordinary income

-

Subject to Required Minimum Distributions

Understanding how Traditional IRA withdrawals are taxed is critical — especially when planning around brackets and RMDs.

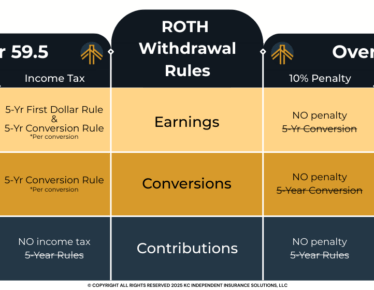

Roth IRA

A Roth IRA is funded with after-tax dollars.

-

No upfront deduction

-

Growth is tax-free

-

Qualified withdrawals are tax-free

-

No lifetime RMDs for the original owner

Roth accounts are often used strategically for long-term tax diversification and bracket management.

Employer-Sponsored Plans (401(k), 403(b), 457(b))

These workplace retirement plans:

-

Are typically funded with pre-tax contributions

-

Grow tax-deferred

-

Are taxed as ordinary income when withdrawn

Many plans now offer Roth options as well.

When evaluating whether to leave funds in a workplace plan or reposition them.

SEP IRA & SIMPLE IRA

Used primarily by self-employed individuals and small business owners:

-

Pre-tax contributions

-

Tax-deferred growth

-

Taxed as ordinary income upon withdrawal

Health Savings Account (HSA)

Often overlooked in retirement planning, the HSA can be one of the most tax-efficient accounts available.

HSAs offer:

-

Pre-tax contributions

-

Tax-deferred growth

-

Tax-free withdrawals for qualified medical expenses

This is often called triple tax advantage.

Unlike other retirement accounts, HSAs are not subject to required minimum distributions, making them powerful for healthcare cost planning in retirement.

Why Understanding Account Types Matters in Retirement

Many retirees discover that the majority of their savings are in pre-tax qualified accounts. While tax deferral is helpful during working years, it can create challenges later:

-

Larger Required Minimum Distributions

-

Higher taxable income

-

Increased Medicare premiums

-

Greater exposure to future tax rate changes

Having a mix of qualified and non-qualified funds — and potentially Roth dollars — allows for more strategic income sequencing.

Where Hybrid Pensions Fit In

At KCIIS, our focus is on helping clients turn their retirement savings into a reliable, pension-like income they cannot outlive.

One strategy we introduce is what we call a Hybrid Pension — an annuity-based solution designed to provide:

-

Guaranteed lifetime income

-

Principal protection

-

Reduced market volatility exposure

-

Potential tax efficiency

-

Long-term care planning integration

Hybrid Pensions are not meant to replace traditional retirement accounts. Instead, they work alongside them to create predictable income while reducing uncertainty in retirement. Our goal is to help clients understand how all of their accounts fit together so they can retire with greater clarity, confidence, and control.

How Hybrid Pensions Are Taxed

Taxation depends entirely on the source of funds used to fund the contract:

If Funded with Qualified (Pre-Tax) Dollars:

-

Withdrawals are generally taxed as ordinary income

-

Similar to Traditional IRA or 401(k) distributions

If Funded with Roth Dollars:

-

Income may be tax-free if Roth rules are met

If Funded with Non-Qualified Dollars:

-

Earnings are taxed first (LIFO rules)

-

Principal is returned tax-free

Understanding this distinction is critical to building tax-efficient retirement income.

Which Account Type is Best?

The simple truth is that there is no single “best” retirement account.

The goal is to have the right mix of account types that work together to:

-

Manage tax brackets

-

Reduce lifetime tax exposure

-

Provide income stability

-

Improve flexibility

-

Protect against market risk

Understanding how retirement accounts are classified is one of the most powerful steps toward retiring with clarity, confidence, and control.

If you’d like to explore how your qualified and non-qualified accounts could work together in a retirement income plan, you can begin here

Contact Us Get in Touch

Have a question or feedback?

Fill out the form below, and we’ll respond promptly!

By providing your name and contact information, you are consenting to receive calls, text messages, and/or emails from a licensed insurance agent about Medicare Plans at the number provided. You agree that such calls and/or text messages may use an auto-dialer or robocall, even if you are on a government do-not-call registry. This agreement is not a condition of enrollment.

Not connected with or endorsed by the United States government or the federal Medicare program. This is a solicitation of insurance, and your response may generate communication from a licensed producer/agent.