How We Help Clients Retire Early Using Hybrid Pension Strategies

One of the most common reactions we get when introducing a retirement strategy that offers 10% to 20% guaranteed lifetime payouts is, “That sounds too good to be true.” Most people are familiar with annuities that only provide 5% to 7%. But when we show our clients how we structure hybrid pension annuities using staging and laddering, the results speak for themselves. Let us walk you through how it works—and more importantly, why it works.

What Is a “Hybrid Pension”?

A hybrid pension is a fixed-indexed annuity with a lifetime income rider. Unlike traditional pensions, these plans keep your money accessible. If you change your mind or pass away, unused funds can go to your beneficiaries. There are two main types of income riders:

- Contractual Riders: These come with a fee (around 1%) but offer guaranteed roll-ups and predictable lifetime payouts.

- Hypothetical Riders: No fees, but your future income depends on market performance—too unpredictable for our comfort.

We help clients structure these hybrid annuities in a way that unlocks double-digit payouts—but only when the timing and funding are timed strategically.

The Strategy: Staging + Laddering

To achieve those higher payouts, we use a two-part approach:

- Staging

We plan for clients to rely on other income sources, such as savings, brokerage accounts, part-time income, Roth IRAs, or cash-value life insurance in the early years of retirement. Staging annuities buys us time to defer annuity payouts, which is where we see the real magic happen. - Laddering

Instead of starting one annuity, we help clients create multiple smaller annuities, each scheduled to begin at different ages (say 60, 65, and 70). This laddered approach:- Fights inflation

- Provides flexibility

- Unlocks payouts up to 10–20% of the original investment

Here’s an example:

If you deposit funds into an annuity at age 55 and defer income until 65, your payout might be 14.9% annually for life. The longer you wait, the higher the income stream—guaranteed.

The Five Retirement Stages: How We Build the Income Bridge

To make this all work smoothly, we plan your income in five tax-smart stages:

- Stage 1 – Hybrid or part-time work: Light work or other non-guaranteed income (e.g., real estate, dividends).

- Stage 2 – Savings and CDs: Often overlooked, but ideal for bridging the income gap with minimal taxes.

- Stage 3 – Long-term capital gains bucket: If your income is low enough, you may qualify for 0% capital gains tax.

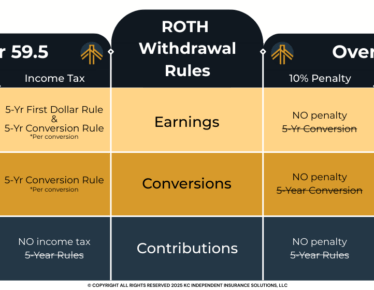

- Stage 4 – Tax-free buckets: Roth IRAs and life insurance cash value accounts. These can fund early retirement while annuities continue growing.

- Stage 5 – Traditional IRA or 401(k): Often the last bucket we touch to reduce future RMD taxes.

Why Most Advisors Miss This

Let’s be honest—most traditional financial advisors don’t talk about these strategies. There are a few reasons:

- Insurance agents often don’t understand the broader tax and income planning picture.

- Financial advisors may not be trained in annuity design or may be reluctant to reduce assets under management.

We take a holistic approach that considers all income sources, tax brackets, and timing decisions because retirement isn’t just about products. It’s about building a customized cash flow plan that works for your goals.

Is It Too Late or Too Early for You?

We’ve helped clients in their 50s stage early retirement while deferring annuity income. We’ve also helped people in their 70s set up late-stage ladders to cover long-term care and RMD concerns. Whether you’re just starting to plan or actively preparing for retirement, it’s never too early to ask: How can I structure my income to last a lifetime—and keep more of it in my pocket, not the IRS’s?

Let’s Explore What This Looks Like for You

If this sounds like something you’d like to explore further, we’re here to help. We work with over 50 annuity providers nationwide, and every strategy we recommend is tailored to fit your lifestyle, risk tolerance, and long-term vision.

Let’s schedule a time to walk through your options.

We’ll show you how the numbers work—side-by-side with your current plan—so you can decide if staging and laddering a hybrid pension makes sense for your future. Let us help you retire not just comfortably, but confidently, with a plan that truly pays off.

Contact Us Get in Touch

Have a question or feedback?

Fill out the form below, and we’ll respond promptly!

By providing your name and contact information, you are consenting to receive calls, text messages, and/or emails from a licensed insurance agent about Medicare Plans at the number provided. You agree that such calls and/or text messages may use an auto-dialer or robocall, even if you are on a government do-not-call registry. This agreement is not a condition of enrollment.

Not connected with or endorsed by the United States government or the federal Medicare program. This is a solicitation of insurance, and your response may generate communication from a licensed producer/agent.